In this in-depth presentation, we embark on a journey through the labyrinthine landscape of ARR calculations, meticulously dissecting various methodologies, providing illustrative explanations and engaging in a discourse on the merits and drawbacks of each strategy. By the end of the journey, you will have a firm understanding of the intricacies that underlie ARR calculations, enabling precise optimization of your company’s financial valuations.

ARR serves as an overarching metric that represents the predictable revenue stream of subscription-based businesses over a one-year period. Unlike GAAP measures, which refer to historical financial data, ARR is a forward-looking barometer used to evaluate a company’s financial performance and forecast future revenue streams. This distinction underscores the forward-looking nature of SaaS companies, for example.

Navigating the terrain of calculations: Methodological considerations

The basic formula for calculating the ARR may seem straightforward at first glance:

Some companies choose to calculate the ARR as 12 times the MRR (MRR = Monthly Recurring Revenue) as a practical alternative, as this is simple and efficient, especially for companies working with monthly subscription models:

ARR = 12 * MRR

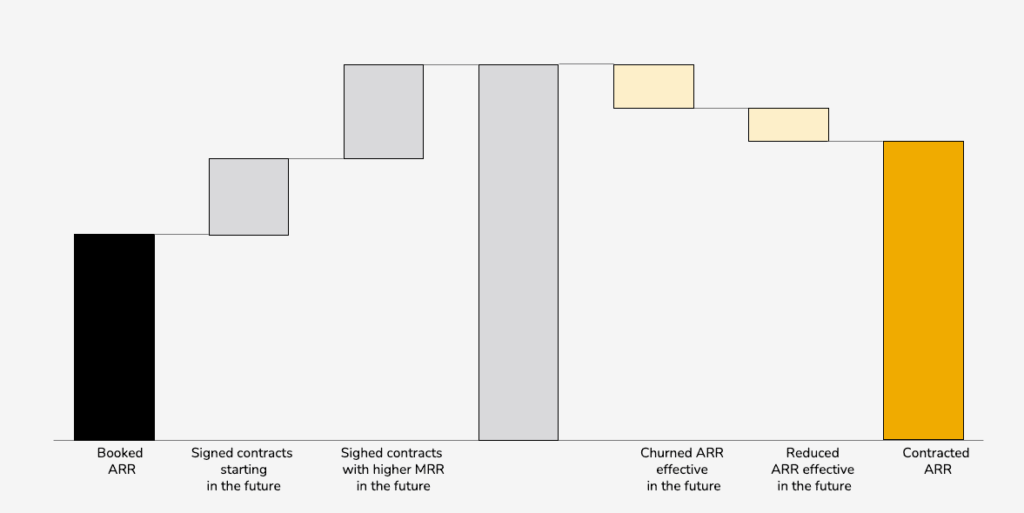

Building on the ARR, subscription companies also like to report the “Contracted ARR” as a measure of sales success based on the subscription contracts already concluded that will only start in the future vs. the recurring revenues that will be lost in the future due to contract terminations or reduced payments.

However, applying the basic ARR formula to real-life scenarios can be very complex, even if currency effects are excluded from the analysis for the time being.

Let’s go through the 9 most common hurdles that also apply to the “Contracted ARR”:

1) Services: Include or exclude recurring service add-ons

Benefits:

- Enables a clear distinction between core subscription revenue and additional services.

- Simplifies the ARR calculation by focusing exclusively on the basic subscription component.

- May inadvertently underestimate total revenue potential, especially if professional services are a significant contributor to the organization’s recurring revenue.

- Does not capture the entirety of revenue from bundled subscription and service offerings.

2) Different contract terms: Include annual and multi-year contracts or those with shorter contract terms

Benefits:

- Prioritizes long-term revenue commitments, providing a more accurate representation of predictable revenue.

- Consistent with the resilience and continuity that characterize subscription-based businesses.

- Disregards projected revenue from shorter-term contracts, which can represent a significant portion of the customer base. Contracts are often renewed on a monthly basis, for example, with revenue per month possibly even increasing.

- May underestimate the immediate impact of monthly subscriptions on the company’s financial position.

3) Projected versus confirmed revenue: Inclusion of delayed renewals in the ARR

Benefits:

- Provides a conservative estimate of the ARR by only considering existing contracts that have been officially renewed.

- Reduces the risk of overestimating revenue from expected renewals that may not materialize.

- Could underestimate actual ARR if historical data indicates a high probability of delayed renewals.

- Neglect of revenue that is highly likely to come from upcoming renewals.

4) Inclusion of expected but not yet confirmed renewals in the ARR calculation:

- Provides a more optimistic and holistic view of ARR as potential revenue from expected renewals is included.

- Provides a more accurate representation of the company’s revenue potential, especially in cases characterized by a high renewal rate for late contracts.

- Involves a degree of uncertainty as expected renewals do not always materialize, potentially inflating revenue estimates.

- Requires a comprehensive understanding of customer renewal patterns and reliable data for accurate forecasting.

5) Exclusion of usage-dependent sales

- Simplifies the calculation process by focusing exclusively on basic subscription sales.

- Avoids potential complexity and inaccuracies arising from variable usage fees.

- May not reflect full revenue potential, especially if usage-based revenue and consistent overages play an important role in the organization’s revenue stream.

- A key aspect of revenue generation is not considered, which may result in an incomplete financial assessment.

6) Inclusion of usage-based sales

- Provides a comprehensive view of revenue by including both base subscription fees and additional revenue from usage fees and consistent overages.

- Reflects the actual revenue potential, especially in scenarios where usage-based pricing has a significant impact on the company’s financial position.

- Introduces unpredictability as usage fluctuations can make revenue more variable and difficult to predict, potentially impacting ARR and complicating financial projections.

- The inclusion of usage-based pricing and overages can increase the complexity of the billing process, which can lead to errors.

- Control of customer activation dynamics: inclusion or exclusion of contracted but not yet active customers from the ARR calculation

7) Exclusion of contractually bound but dormant customers from the ARR calculation:

Benefits:

- Enables a conservative ARR estimate, as only customers who actively use the product or service are taken into account.

- Reduces the risk of overestimating revenue by excluding potential customers who do not activate their contracts.

- May underestimate revenue potential in scenarios characterized by minimal time intervals between contract signing and go-live combined with a high probability of activation.

- – Does not capture expected revenue from contract customers who are about to activate their subscriptions.

8) Treating early renewals that overlap with existing contracts as separate contracts without extending them:

Benefits:

- Maintains a clear distinction between existing and renewed contracts, enabling better tracking of revenue streams.

- Minimizes potential confusion or overlap in revenue allocation during renewal epochs.

- May not accurately reflect the continuous revenue stream from early renewals that overlap with existing contracts.

- Requires close monitoring to ensure accurate tracking and reporting of overlapping renewals.

9) Extend early renewals that overlap with existing contracts and combine into a single contract:

- Provides a more comprehensive view of revenue by recognizing the longer commitment and continuity associated with early renewals.

- Reflects actual revenue generated during overlapping renewal periods, ensuring accurate financial valuations.

- Requires meticulous analysis and consideration of contract terms and renewal periods to accurately determine extended revenue.

- Can complicate tracking and reporting during overlapping renewal periods.

ARR vs. contracted or committed ARR

It is important to note that CARR is a snapshot in time, comparable to a balance sheet item, as opposed to turnover, which covers a specific period of time. CARR can be reported at any point in time, whereas sales figures must relate to specific time periods.

Conclusion: Preparation for any due diligence by professional investors

It is important for investors to maintain a consistent definition to ensure comparability over time. The selected definitions should always be stored to ensure the necessary traceability. It is also essential to automate reporting in order to avoid calculation errors.